Mobile payment four modes comparison

When the mobile Internet has developed four times faster than the Internet, mobile payment has evolved into a battleground for military companies. On the other hand, with the three major operators successfully catching up with third-party payment licenses at the end of 2011, mobile phone card consumption has become a new gold nugget in the communications and financial industry.

The remote payment and the near-field payment are interlaced, and the mobile payment market is accelerating. With the scale of more than 900 million mobile phone users and the gradual maturity of 3G technology, the attractive market prospects of China Mobile Payment have brought new interest games to banks, operators and third-party payment companies. The industry believes that mobile payment, which is still in the market cultivation stage, will be led by remote payment this year and will be led by third-party payment vendors. Telecom operators and banks have natural advantages in near-field payment, but the two standards are disputed. And the popularity of cross-industry integration applications has yet to be resolved.

Remote payment leads the way

At the end of 2011, China Mobile, China Unicom and China Telecom, which had 900 million users, were finally selected for the third batch of third-party payment licenses. The payment companies of the three major telecom operators have obtained two business licenses for mobile phone payment and bank card receipt. With the business advantage of fixed-line telephones, Telecom’s Tianyi e-commerce and China Unicom Woyi paid a fixed-line payment. license. Previously, the joint advantage of China Mobile and China UnionPay's joint venture company has also been licensed, with two licenses for Internet payment and mobile phone payment.

The entry of operators has led to new changes in the field of mobile payments. Telecom operators have operational experience and huge channel coverage in the field of communication technology; banks as the ultimate payment clearing institution have an advantage in payment clearing management and user scale; third-party payment vendors have accumulated rich experience in the field of Internet payment, each of which has its own Advantages, market competition is becoming increasingly fierce.

Currently, mobile payments are divided into remote payment and near-field payment. Among them, remote payment allows the user to log in to the bank's webpage or the client through the mobile phone to perform payment and other operations. In the near field payment, the mobile phone transmits the local communication with the terminal device such as POS through the transmission modes such as radio frequency, infrared, and bluetooth.

Analyst Zhang Meng of Analysys International believes that mobile payment is still in the stage of market cultivation, and it still needs to wait 2-3 years for the outbreak period. "And remote payment as a mobile Internet-based online payment, the industry chain is relatively simple and clear, and third-party payment vendors in the Internet online payment field for 10 years of payment operation experience, remote payment will take the lead."

The data shows that in 2011 China's mobile Internet market reached 39.31 billion, an increase of 97.5% year-on-year, of which mobile e-commerce transactions grew rapidly, accounting for 29.2%, and is expected to become the largest segment by 2012. "Mobile Internet-based applications will become more and more abundant. In addition to games, videos and other mobile entertainment applications, public utility contributions, online banking, airline hotels and mobile e-commerce, which are closely related to user life, are gradually transferred from PC to mobile phones. With the mobile side, the development of these transactional mobile applications is becoming more and more urgent for mobile payment, which brings huge market space for remote payment." She believes that, relatively speaking, near-field payment is to integrate account information into mobile phones. At present, it is still in the stage of micropayment, and the application scenarios are still limited to public transportation, independent large-scale parks, universities and so on.

How third-party payments skip hardware barriers

In fact, before the operators got the license, Alipay, fast money, and remittance world had already pre-empted the mobile payment market. In 2011, Remittance World officially released a mobile payment strategy called “Asi@â€, which invested 100 million yuan to deploy mobile payment, providing mobile Internet-based full payment settlement and capital chain management solutions for the upstream and downstream of the industry chain.

Mr. Zhou Wei, Chairman and President of Remittance World, told the Southern Reporter: “Mobile payment is a historical opportunity to change the structure of the payment industry. It is expected that the mobile payment in the world will reach 100 billion yuan in 2012.â€

And Alipay launched a bar code payment and two-dimensional code payment. Alipay public relations personnel told the Southern Reporter that after installing the mobile Alipay client, the user can form a random barcode, and the merchant can use the mobile phone or barcode gun to scan and realize the payment between the merchant and the consumer. “The installed volume of Alipay mobile phone clients has reached 10 million, and the daily transaction volume from wireless has reached 500,000.â€

The fast-moving “quick brush†products have entered the commercial stage. According to Wang Hao, the director of fast money public relations, this plug-in device can be used as a mobile PO S machine to cover remote payment, mobile payment and other functions after inserting the external device into the mobile phone.

The development of mobile payment is closely related to the construction of a complete industrial chain. At present, China Mobile's operation at the 2.4GHz standard coexists with the 13.56MH payment standard promoted by China UnionPay. The transformation of the citizen's mobile phone and merchant hardware is subject to cost and technology, stagnating, making it eager to share the mobile payment cake. The person has to find another way.

Zhang Meng said that the current common products for remote payment are divided into "independent client" and "in-app payment", which are mainly developed and designed by third-party payment vendors. Independent client payment is mainly for the loyal customers of the payment platform, and has a relatively large user base, such as Alipay and Tenpay. Most of the third-party payment vendors that are mainly for enterprise customers do not have the advantage in personal payment. In-app payment is embedded in the application through the middleware, and the user does not have to leave the current page in the payment process. “Bar code payment, audio plug-in card payment, in fact, is a transitional solution when the in-app payment has not reached a certain level of popularity.â€

Earnings outlook is not clear

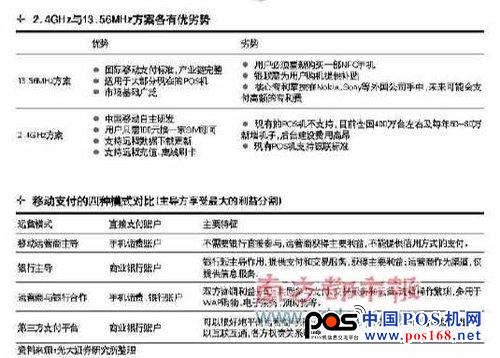

At present, there are four main business models for mobile payment, namely, the operator-based operation mode; the bank-based operation mode; the bank-operator cooperation mode, in which the operators only provide information. The channel to be transmitted; the last is a mode of operation dominated by third-party payment service providers, mainly focusing on remote payment. Zhang Meng said that no matter which business model, there are only three main profit models: forward service fee, settlement fee and post-business service fee.

"Mobile payment is currently in the early stage of development, with investment as the main factor. The first benefit is definitely the manufacturers in all aspects of the industry chain, and the profit prospects of enterprises based on providing payment operation services are still unclear." Zhang Meng said.

At the end of last year, the Ministry of Industry and Information Technology said that it has started the development of mobile payment standards with the central bank. The internationally popular 13.56MHz solution and the domestic proprietary intellectual property 2.45GHz solution will be included in the industry standards. Among them, China Mobile adopts the 2.4GHz standard RF-SIM full card solution, the main obstacle is to change the high investment of POS machine.

Everbright Securities analyst Zhou Liqian said that each solution of mobile payment faces high investment, and the short-term interest space is small, but in the field of mobile payment, companies that enter and can quickly achieve business coverage can form a high entry. threshold. While the three-party payment platform such as Alipay and Tenpay is relying on a large number of existing customers such as Taobao to achieve rapid development, it must cooperate with China Mobile, which also has a large number of customers, to coordinate the distribution of interests in order to achieve long-term in the mobile payment market. development of.

Related reports

China Mobile, UnionPay, each killer

Recently, the three major domestic operators have finally obtained the long-awaited mobile payment license, and successfully “certified to workâ€. Different from other licensed institutions, basic telecom operators, especially China Mobile, have become more and more aware of the “ambition†of mobile payment. The industry expects that its 2.4GHz standard will coexist with China UnionPay's 13.56MHz payment standard. It is understood that the current 2.4G Hz standard is mainly used on mobile phones. At this stage, it is impossible to interconnect with the terminal POS of UnionPay. Both standards have their own merits, and the weak and weak will affect the direction of the entire industry chain. After the obstacles have been smoothed, the two standard games have become the next point of view for the development of mobile payment in China.

Operators participate in the war, two standard games

The standard dispute has always existed. Behind the competition for different standards is the game of interest groups. UnionPay and telecom operators all hope to compete for their dominance in the mobile payment industry through their own standards. Xie Yuqi, Director of the Policy Standards Division of the Communication Development Department of the Ministry of Industry and Information Technology, said that the coexistence of multiple standards has created obstacles for large-scale application of mobile payment.

The 13.56MHz payment scheme favored by UnionPay is an international mobile payment standard. The patents are controlled by international giants such as Nokia and Sony. They are used more internationally and have mature development. They are widely used in non-contact card fields such as transportation, finance, social security and fueling. For most existing PO S terminals; however, its shortcomings are obvious. First, the user's mobile payment service must be replaced with a carrier-specific mobile phone and SIM card; secondly, the signal is susceptible to metal structure, to ensure the strength of the signal, the mobile phone The back cover cannot use metal; again, it does not support remote recharge.

As for the 2.4GHz mobile payment solution of China Mobile, the user only needs to replace a special payment SIM card with radio frequency to realize the payment. Even if the mobile phone is replaced, the card can continue to have the mobile payment function. However, as the domestic domestic independent research and development products, China Mobile's first product, its industrial chain is not yet mature, because the frequency of work is inconsistent with the POS machines of major industries such as banks and public transportation, the terminals need to be re-laid or modified, which requires public and Coordination between the financial sector and telecom operators requires a certain amount of work and a large cost. According to estimates by Everbright Securities, there were a total of about 3.33 million POS machines nationwide at the end of 2010. Assuming a POS machine costing 2,000 yuan (below the market price), a total investment of 6.66 billion yuan is required.

Advantage areas have their own advantages

The current reality is that the 13.56MHz standard represents the international advocacy standard, with high maturity and rich commercial experience; the 2.4G standard has the function of swiping cards, no restrictions on mobile terminals, and better scalability in the future. As a result, the result is that the terminals that make short-range payment mostly use the 13.56MHz standard, which means that if you need to use the 2.4GHz standard, you must replace the POS machine and other devices. If you use the 13.56MHz standard, you must Change the mobile terminal and SIM card.

In this regard, Guojin Securities released a research report that compared to the 13.56MHz program, the 2.4GHz program has an inherent advantage in promotion. After all, the 13.56MHz solution must be redesigned for the mobile phone. It needs to wait for the mobile phone industry chain to gradually support 13.56MHz, and the time period is longer. At the same time, the replacement cost brought by replacing the 13.56MHz mobile phone is assumed by the user or by the operator. It is a high cost and it is difficult to promote. And 2

Home and Office Table series are big series and multipurpose that it includes Side Table, Laptop Table, Computer Table and so on.Those can be used for Office and Home.Material also can be wood, MDF, steel frame and so on different on different customer`s requirement.

HEALTH AND WELLNESS: Standing Desk encourages greater movement throughout your day while helping optimize your cognition, improve focus, enhance collaboration, reduced back and neck pain, increase productivity and boost calorie burn.

Office Desk, Executive Desk, Standing Desk,Home Office Computer Table

Foshan Hollin Furniture Co.,Ltd , https://www.hollinfoshan.com